Well. It happened. The bear market that we’ve been saying was at our doorstep for years is finally here. The pandemic that scientists warned could cripple our society has come. While writing this I am on my fifth day of quarantine and the world outside is starting to feel a bit like a post apocalyptic film.

So what am I going to do about it?

For starters, I am going to stay the hell inside, wash my damn hands, and stay educated on what authorities such as

WHO– The World Health Organization

CDC– Centers for Disease Control

and my local department of public health have to say about this.

But what about financially?

As I mentioned in this article I am currently on sabbatical through this Summer. Since I financially planned for this heavily, I have a pretty bodaciously large emergency fund. Normally we would keep just 3 months of expenses in our high interest savings account, but, with both me and Mr. Hippie temporarily out of the workforce to spend time with creative projects, we conservatively bumped this up to about 1 year. Due to some unpredicted income through a grant, side hustles, and some other miscellaneous sources, I’ve actually added about 3.5 month’s worth of expenses to that pile (What can I say? Apparently I like earning money even when I tell myself not to.) So, we are still set cash-wise to weather the storm for another 9 months or so without touching our investments or earning another penny in income. That runway could honestly even be longer now since we have had to cancel half a dozen different trips and excursions over the next couple months and I don’t foresee quarantine life being particularly expensive.

In spite of how set we are, I’m still motivated to try to tighten my belt a bit more in times of economic uncertainty and reduce my expenses. Since we won’t be traveling or leaving the house much for the foreseeable future, we did recently score a new internet plan with a new provider in our area which will save us about $25/month while getting the same speeds.

For food, I am sticking to my low-cost, shelf-stable staples:

- Oats

- Rice

- Dried black beans

- Dried chickpeas

- Quinoa

- Tuna

- Lentils

- Pasta

I’m also working on expanding my backyard garden to produce fresh food which will hopefully reduce my grocery budget and, perhaps more importantly right now, reduce my need to leave the house to go to the grocery store. I already have kale, chard, mint, and leeks planted in my backyard and have recently dedicated around 10 hours of digging to create a new bed for squash.Gardening is one of my strategies to get outside and remain active during this period of quarantine.

All this to say, I will continue to pull from that cash pile and will not under any circumstances be touching my IRA, 401k, HSA, or taxable accounts. I last logged into Personal Capital about a week ago and won’t be checking it again until the end of the month when I update my spreadsheets. The market will eventually recover, and I know that downturns like this are built into that ~7% annual return estimate. But, knowing it and not internalizing any stress from seeing the numbers drop are two entirely different things. To keep my mental health in the best place, I am placing my trust in the Hippie of the past who set the appropriate allocation based on my age, risk tolerance, where I am in the FIRE path, and my withdrawal strategy. She knew what she was doing.

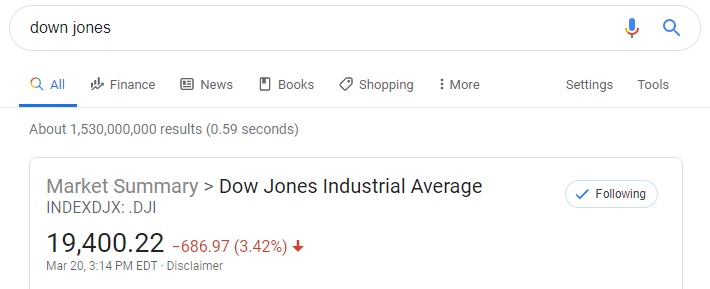

I can conservatively say my portfolio is definitely down at least 6 figures though, and seeing the DJI continue to drop does make me itch to start earning a little more and beefing up my accounts. When I updated my spreadsheets in mid-February we were within a couple years of our FIRE number if we both took positions at our old salaries and continued to keep up our 50%+ savings rate. Had we stuck with Coast FI or Barista FI, we would have reached it within a little over a decade. I have to assume those numbers are going to be heavily extended at this point, which is part of what has me eager to jump back into the workforce this Summer to start cutting down on that horizon.

Mr. Hippie and I reached a deal once we got to around 50% FI that we will each earn at least 25k/year minimum until we are fully financially independent. This is very different from what our salaries were prior to reaching this milestone, but hitting 50% FI was around the time when we realized how much our money was going to start growing even if we didn’t continue to contribute to it. We landed on this specific 25k number because it’s enough to cover our expenses annually with usually quite a bit leftover. This enables us to have the luxury to have a lot of options to earn this income. We could do lower-paid-yet-more-meaningful work, part-time work, or even freelance work if we wanted. We could also work on personal projects that are a bit more risky in terms of their profitability such as self-employment. We are extraordinarily committed to living happy, content lives filled with joy where we can responsibly take our careers and how we spend our time in any direction we like and we no longer feel obligated to work full-time positions we hate.

Ultimately, the market dropping 30% won’t really change that. If we decide to use this as a time to earn more money and invest further while the market is low, this could be a great opportunity to lean into some of our more profitable passions. I am incredibly grateful and feel very privileged to have such an amazing setup right now. Recently, I received an email telling me that the side hustle I look forward to every month has been cancelled until further notice. While this won’t have a significant effect on me, my thoughts are with those who needed and depended on this money to make it through their lives and avoid going into debt.

While this article touches only on my own financial plan for weathering the crisis, I’ll be writing more about how this pandemic is affecting society at large in other posts. Let me know how you’re doing in the comments or on Twitter and stay tuned for future posts.